This blog helps define what virtual accounts (VAs) are, provides a distinction between the two main types of VAs, and then examines each’s various use cases within the corporate treasury arena in 2022. After evaluating the potential benefits and drawbacks for enterprises when incorporating virtual accounts, we conclude by providing helpful tips for treasury to consider before implementing them and highlight how TIS’ solution can supplement their usage by providing advanced bank connectivity, payments, liquidity, compliance, bank account management (BAM), and security capabilities.

Virtual Accounts 101: A Quick Refresh

For those who may be unfamiliar or need a refresh, there are two primary types of virtual accounts that corporates and enterprises use today.

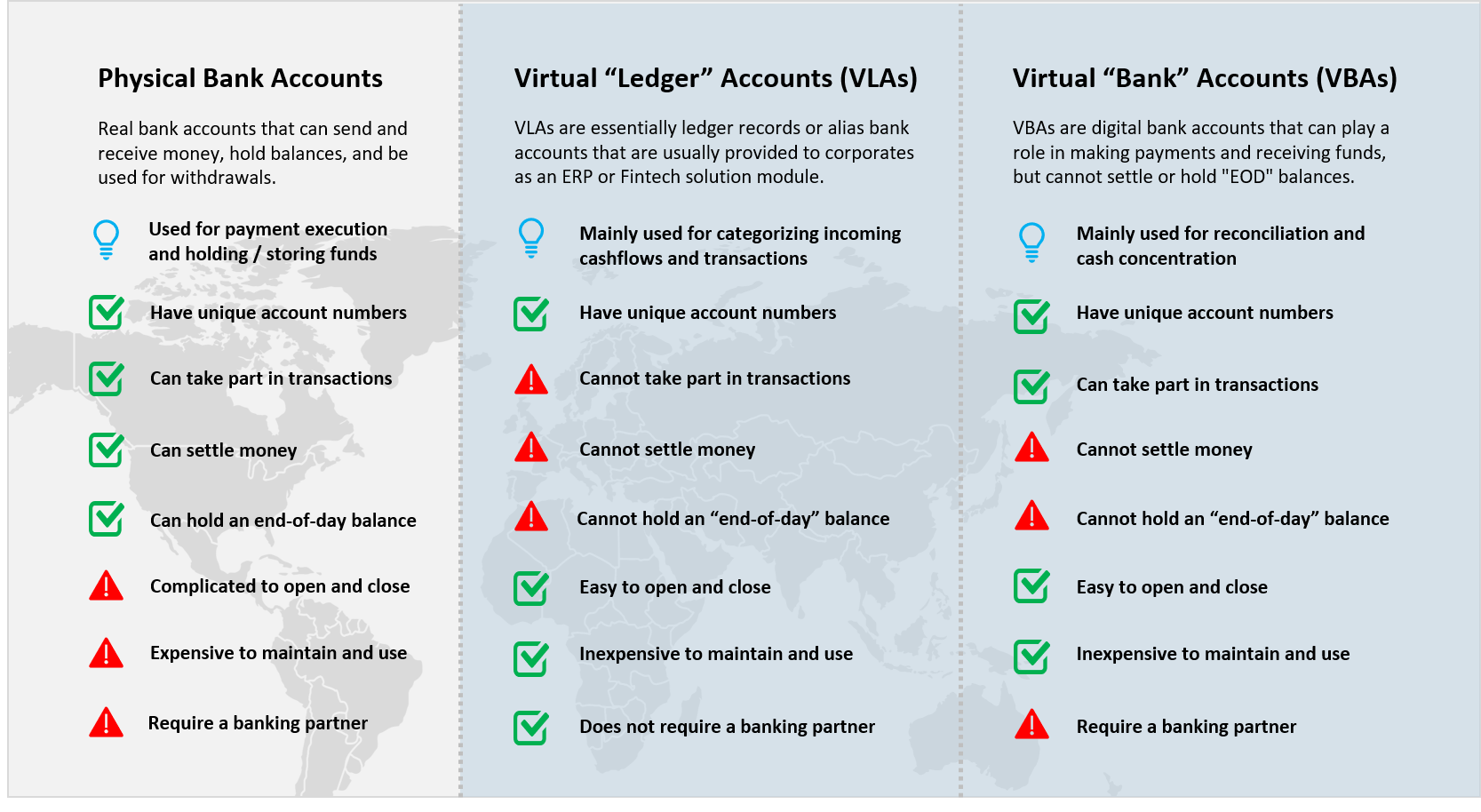

1. VLAs: The simplest form of modern VAs are virtual “ledger” accounts (also known as VLAs or “shadow” accounts), which are essentially just ledger records or alias bank accounts. Typically, VLAs are provided to corporates as a software package by fintech vendors or as a module of their ERP system. They are also typically part of a treasury or in-house bank solution. Financial institutions can also host VA software on behalf of their corporate clients via a cloud-based, online portal.

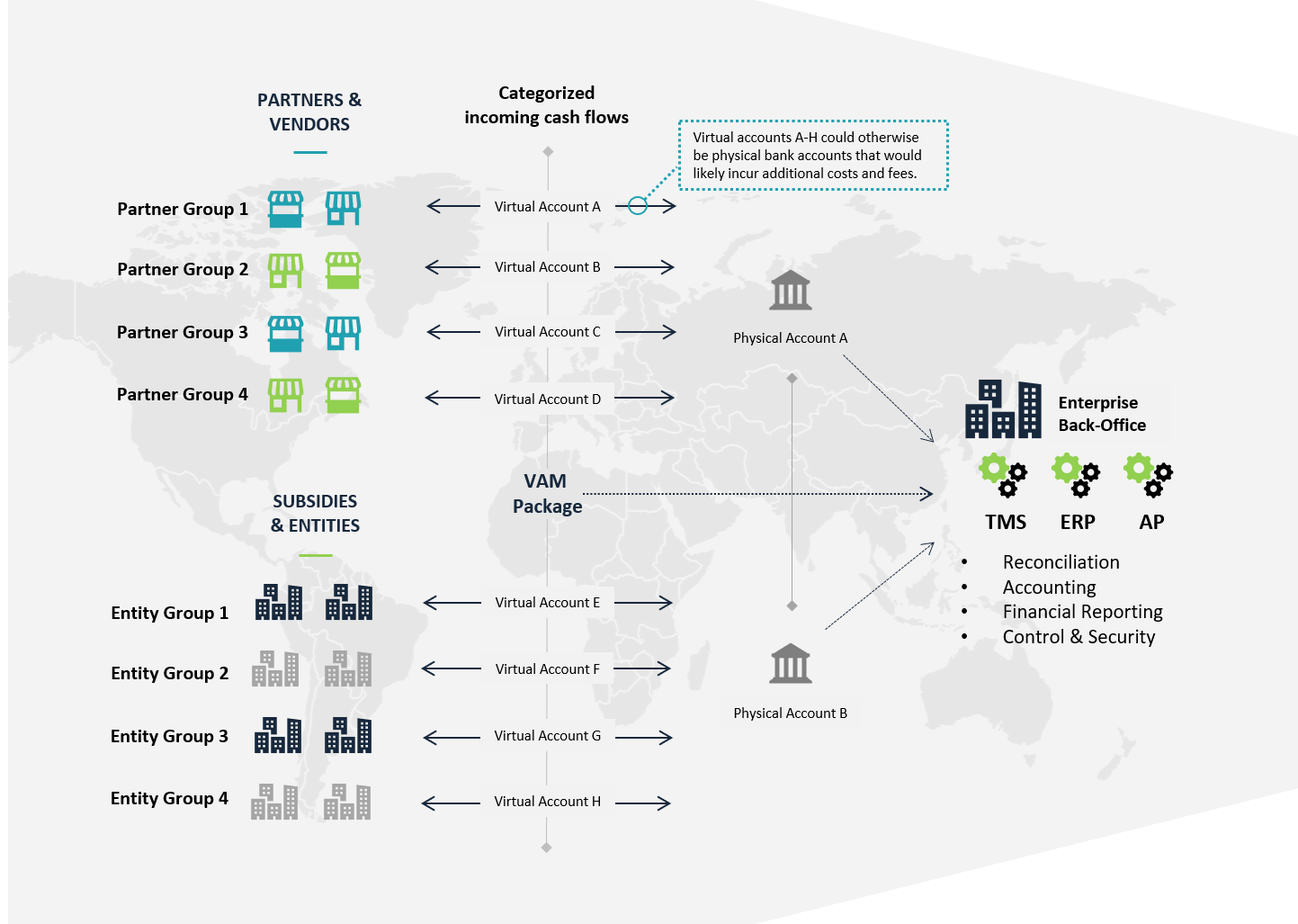

The primary use case for VLAs is to help sort incoming cashflows and transactions as they enter a current or “standard” operating bank account. A helpful analogy for understanding VLAs is to think of them as doors that lead into a series of rooms, with physical bank accounts serving as the rooms that they lead into. Just as a door cannot hold people, VLAs cannot hold or settle money and do not play any legitimate role in the actual transaction. However, in the same way that doors are used to direct people into the right room of a house or building, so VLAs are used to track and record funds as they pass into various physical accounts at an enterprise.

2. VBAs: Virtual “bank” accounts (VBAs) are a slightly more sophisticated type of service. VBAs are used to transact on behalf of a real, physical bank account. Although virtual bank accounts have unique account numbers and can play a role in transactions similar to physical accounts, they compare with VLAs in the sense that they cannot hold an end-of-day balance or technically settle money. Instead, they can only support the pass-through of transactions between other real bank accounts.

However, because VBAs can take part in transactions and are technically “owned” by a specific entity (i.e., enterprise treasury, a subsidiary, etc.) a bank must do the required due diligence (e.g., KYC), as if it were a regular current account. Although this may add more complexity to using them, it also provides more functionality. As noted, VBAs are primarily used to support enterprise cash concentration, and can also be very beneficial for reconciliation.

Today, the benefits of using VBAs as compared to actual current accounts are particularly useful for large (usually multinational) organizations. This is because they help finance and treasury personnel manage functions like reconciliation, cash concentration (a type of automatic cash pooling), repatriation, and accounting, especially if there are a limited number of legal entities in certain jurisdictions due to compliance. And because both VBAs and VLAs are less expensive to open and maintain than current or standard operating accounts, they often represent an opportunity for cost savings.

For instance, a treasury group operating at the headquarters of a large, multinational company may create a series of virtual accounts to help categorize incoming cash flows from certain clients, entities, countries, currencies, or banks. By creating and assigning virtual accounts in an orchestrated manner, treasury can more easily monitor cash flows and transactions across different business segments, even if money is flowing into one current account from numerous sources and channels.

However, because there are significant tax and legal implications surrounding the use of VBAs and with a broad disparity of both VBA and VLA services across the banking and fintech landscape, how do their associated benefits and advantages compare with their drawbacks and challenges?

Let’s explore further.

Summarizing the Benefits & Use Cases of Virtual Accounts for Corporate Treasury

In 2022, there are a variety of benefits that enterprises can achieve by incorporating virtual accounts into their banking structure. As a brief summary, some core advantages and use cases are highlighted below.

Transaction & Liquidity Management. Perhaps the most common benefit achieved from the use of both VBAs and VLAs is a simplified cash and liquidity management structure. This is because virtual accounts can be assigned to help track and manage transactions that are flowing into a single current account (or even numerous physical accounts), which would otherwise require manual categorization and sorting of transactions. Instead, virtual accounts can be used to categorize incoming cashflows by specific entities, clients, and so forth. And by developing an organized virtual account structure and designating accounts for specific purposes, enterprises can more easily monitor their global cashflows.

Reconciliation & Reporting. As a subsequent benefit of streamlined cash and transaction management, it also becomes monumentally easier for companies to manage reconciliation and accounting with virtual accounts. This is because the virtual accounts are already automating the process of categorizing various transactions and cashflows, and by the time global financial data arrives in an ERP or other back-office system, it has already been organized and sifted.

Banking Cost & Fee Reduction. Because virtual accounts are not “real” accounts, standard bank fees and rates do not apply to them. This means that if treasury groups can substantially replace or substitute real physical current accounts with virtual accounts, they can achieve a significant reduction in bank costs. This use case is often a top priority for organizations operating with hundreds or thousands of physical or current accounts, as the associated cost savings can be substantial. However, there are a few points to keep in mind. While a small number of actual bank accounts may significantly reduce banking fees, you may be facilitating “intercompany loans” through the comingling of cash from different entities in one or more current accounts. This, in turn, can have significant tax implications. In addition, there are legal restrictions in certain jurisdictions regarding POBO or COBO (i.e., making payments or receiving funds of one legal entity on behalf of another). And finally, banks rarely react quickly to requests for closing physical accounts, and the errors associated with such processes can be numerous. Closing accounts means a loss of revenue for the bank, so this activity is usually not prioritized and it can take more time than expected to achieve an account rationalization as outlined above.

Security & Fraud Prevention. VLAs can help with security because organizations have far fewer bank accounts to manage, and they don’t have to give away as much account information to outside parties. In this way, less information is exposed, and the risk of fraud is subsequently lowered. On the other hand, when using VBAs, unique IBANs or account numbers are indeed provided to clients, partners, and vendors. However, there is still less risk because these accounts are not holding or settling funds, and their usage helps significantly with reconciliation.

What are the Potential Drawbacks of Virtual Accounts?

The main drawbacks associated with VBAs relate to the complex and shifting set of regulatory and compliance restrictions that impact their usage – for both banks and corporates – in certain localities. While the use of virtual accounts within a single territory (e.g. the U.S.) may be complicated enough on its own, the degree of difficulty is exponentiated for enterprises that intend to deploy their VBAs across a diverse range of regions and countries.

In most cases, the main regulatory challenge for treasury stems from the fact that virtual accounts and their impact on standard bank accounts are treated very differently from a taxation and legality standpoint by different countries. For instance, organizations that want to use VBAs as part of an in-house banking or cash pooling structure will likely face restrictions across Europe and North America. Today, it is common for countries in these regions to require enterprises to maintain a physical bank account in the territory where sales and revenue are being derived, or to maintain a physical account structure for each enterprise entity and business unit. This can limit the effectiveness of using VBAs for cash concentration and in-house banking, and also cuts back on the potential cost savings. Going a step further, countries like China with very stringent compliance regimes have outright banned the use of virtual accounts, and if more countries follow suit, it will severely limit the utility of VBAs as a global tool.

In addition to these VBA-centric compliance concerns, another significant drawback for both VBAs and VLAs relates to the disparity of services provided within the banking and fintech community. For VLAs, it is typically a fintech, ERP, TMS, or specialty provider that offers software modules to support the service. Some banks have created or adopted white-labeled services as well. However, while there are providers that have developed robust capabilities in this arena, others may not offer any solution at all or only provide barebones services with a few core features. The availability of such solutions also varies widely by country, and because the pricing for such services is broadly disparate across the full landscape of providers, corporates must be prudent when performing their due diligence in order to select the best-fit option.

As a final point, while some of the top global banks offer robust VBA solutions and implementation services, the process of opening and closing accounts is not always straightforward. Some banks may require you to first close the physical accounts you wish to replace before the VBAs can be created, which adds new up-front costs that may cut into projected cost-savings. And as mentioned earlier, because banks are essentially losing money by helping corporate clients replace their physical accounts with virtual accounts, such projects may be a lower priority for them. In addition, some banks provide separate portals for managing physical vs virtual accounts, which adds additional technology complexity for enterprise users and inhibits their ability to maintain unified visibility and control.

So then, taking into account all the pros, cons, and potential use cases for virtual accounts, how should interested treasury groups approach the use of virtual accounts over the next 3-5 years?

Final Thoughts on VBAs & VLAs + Next Steps for Optimizing Your Global Banking Structure

For organizations interested in leveraging virtual accounts, here are three quick tips to help you get started:

1. Review the tax and regulatory requirements in each region you wish to open and use virtual accounts. As noted above, the regulations surrounding the use of VBAs differ widely by region and country. This means that an enterprise’s use of virtual accounts will likely be treated differently in each locality where they are deployed. To avoid repercussions or penalties related to improper usage, it is strongly recommended that treasury consult with tax, legal, and banking experts before implementing virtual account structures, especially if numerous nationalities, regions, and entities will be involved.

2. Perform due diligence on a variety of VBA and VLA providers. Bank and fintech offerings in the VA arena still have a lot of disparity, and certain solutions may focus on entirely different use cases, so it’s important to select a provider that satisfies your unique needs. Take time to understand each bank’s requirements for opening and closing physical vs virtual accounts, how they intend to host the associated software, what the corresponding fees are, and to what extent they can help with configuration and implementation. If you plan on integrating your Virtual Account Management (VAM) solution with an ERP, TMS, or other back-office system, also make sure to inquire about the API or connection-level capabilities of each provider.

3. Developing the right VBA or VLA structure can provide multifaceted benefits. Although there are potential challenges to incorporating virtual accounts, enterprises that can identify the right provider and structure their accounts in a compliant manner stand to achieve significant reward. From cost savings, efficiency gains, and automated reconciliation to heightened security and streamlined liquidity concentration, virtual accounts can be a huge boost not only for treasury, but the entire organization. It all just depends on your company’s unique composition and ability to navigate potential legal, compliance, and technology hurdles.

As a final note, it’s important to remember that while there are a variety of dedicated Virtual Account Management solutions available on the market today, other cloud-based solution providers like TIS can also help track and report on the entirety of an enterprise’s virtual and physical account activity across all their banks, regions, countries, and entities.

To date, TIS can connect to more than 11,000 banks worldwide through a variety of methods like APIs, Host-to-Host, SWIFT, and more. All regional or country-level payment networks like NACHA, ZENGIN, and SEPA are supported as well. And as part of these connectivity capabilities, TIS accommodates the full suite of messaging standards, formats, and translation services that enterprises require, including support for SWIFT MT, ISO 20022, EBICs, BAI2, and 5,000+ other proprietary and local formats.

By providing this unparalleled suite of bank connectivity services, TIS helps enterprises track and manage all their bank accounts and underlying cashflow activity, as well as payments and reporting activity. Because TIS can also integrate with each of an enterprise’s entities and back-office systems, our solution acts as a unified window for viewing, executing, and controlling global transaction and liquidity activity. This includes information on all payments and receipts that pass through any of an enterprise’s associated virtual accounts. In this way, treasury groups can use TIS to track the entirety of their physical and virtual account transaction data, as well as to perform a range of other services related to payments, liquidity, BAM, compliance, and security.

For more information on how TIS can help you optimize your global bank connectivity and financial messaging structure and transform your payments and liquidity management workflows, access our whitepaper library for the latest research. You can also view client case studies and testimonials, employee interviews, product updates, and more on our website. To contact our team, you can choose the option that best suits you here. We hope to hear from you soon!