This article examines the logical progression of treasury’s technology needs as their company scales and expands over time. As enterprises outgrow their use of Excel and bank portals to require more sophisticated technology, learn how treasury can combine an assessment of their internal needs with a thorough review of the technology market to choose the right solution and vendor and take their operations from mostly-manual to fully-automated.

Excel & Bank Portals: The Natural Starting Point for Smaller Companies

If you’ve worked in treasury at a small or medium sized business or have been practicing treasury for some time, then chances are you have experience managing operations with nothing more than Excel, bank portals, and some other basic tools.

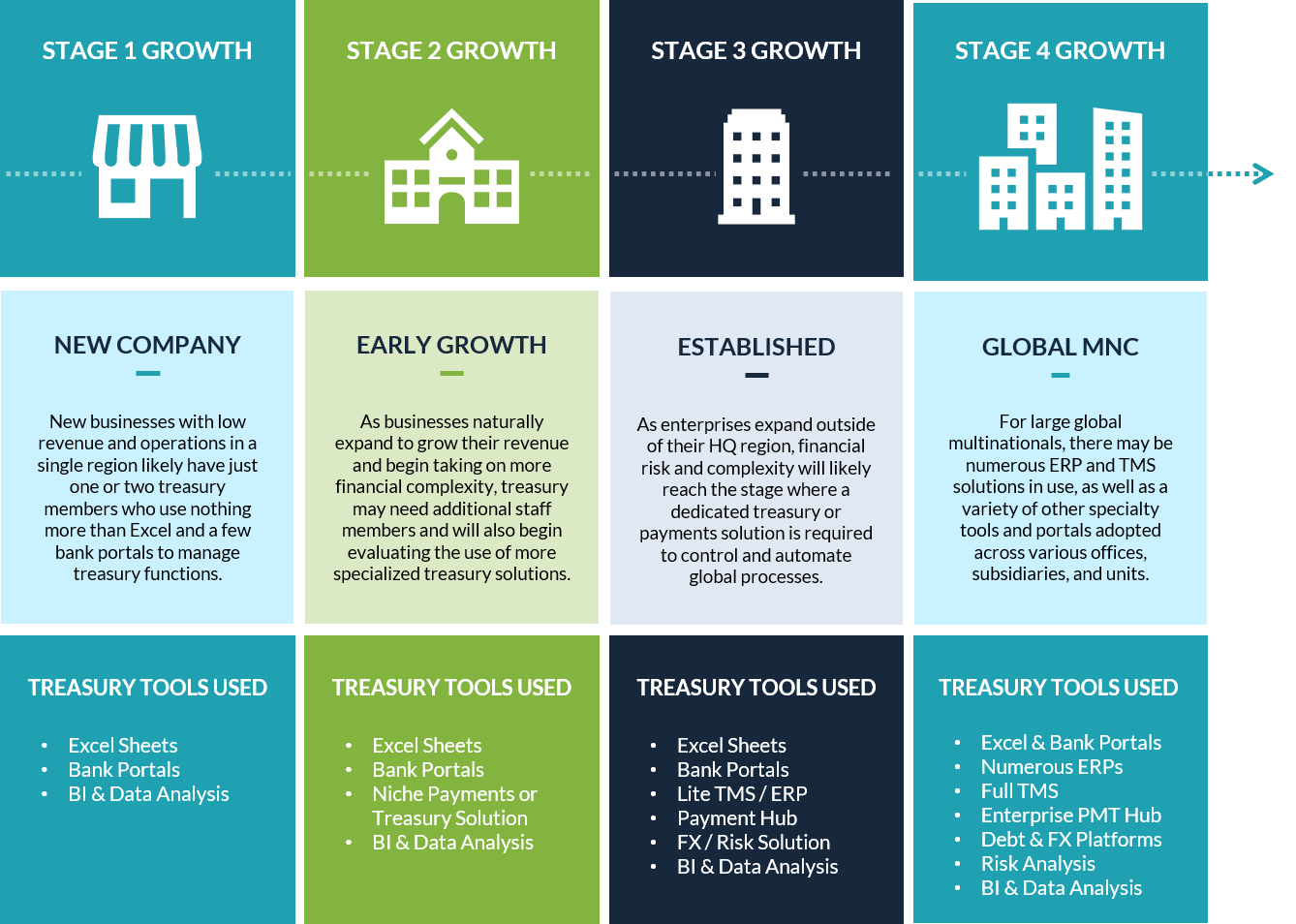

Even today, companies with low revenue, minimal financial complexity, and operations in just a few countries can often get by without sophisticated treasury or payment solutions. Although it’s common for an ERP or CRM platform to be adopted by businesses at early stages in their lifecycle, treasury’s technology needs are rarely prioritized in any meaningful fashion until there is enough financial complexity and risk across the enterprise to warrant an investment.

To be fair, companies that use only a few bank accounts, operate with a single currency, and execute just a few dozen treasury payments each week can probably manage fine without a TMS or similar platform. However, over the course of natural business expansion, there will come a time when simple tools like Excel will not be enough for small treasury teams to effectively perform their operations.

Eventually, new growth opportunities will require their company to expand into new countries, add new subsidiaries, open new bank accounts, add more debt, use more currencies, and make more payments. Investment activity will increase, cash will be more globally dispersed, and forecasting will become more challenging. This will ultimately increase the compliance, security, and risk-related scenarios the company faces as well. And as these new instruments of risk and finance create fresh challenges for managing financial operations, treasury’s processes and underlying technology capabilities will have to evolve accordingly.

How Normal Business Expansion Requires Adjustments to Treasury Technology

Even over the course of just 5-10 years, a rapidly growing company can undergo significant changes that drastically alter the scope of their treasury group’s responsibilities.

Consider the below scenario.

Suppose that a small U.S. company with ~$70mm in annual revenue starts 2015 with all of their business activity occurring inside North America. With only a handful of bank accounts and all finances conducted in USD, the majority of treasury workflows are straightforward and simple. At this stage, the company is executing <100 treasury and supplier payments each week outside of payroll and HR, so individual bank portals can easily accommodate their needs. Daily cash positions can also be quickly generated across the entire company with spreadsheets, and because they do not have any significant debt or investment activity, the need for more sophisticated risk or compliance analysis is low.

However, now suppose that this company experiences rapid growth over the next five years.

In addition to acquiring a new subsidiary in the U.S., this company also expands into Europe through a strategic acquisition of a smaller competitor. At each of these two subsidiaries, there are pre-existing ERP solutions in place, as well as AP and HR systems. Each of these subsidiaries also has a unique set of banks and bank accounts that is different from the HQ company, and the European unit is using a variety of new currencies and payment channels to disburse and collect funds. This European unit is also operating under a jurisdiction with unique compliance and risk-related factors, which adds additional complexity for the HQ treasury team in the U.S.

New growth opportunities related to these acquisitions have also seen the company make substantially more revenue, but also take on more debt and investment activity, much of which falls under treasury’s purview.

In this scenario, the U.S. company’s operations have expanded internationally and taken on significant amounts of new risk and complexity in a short amount of time. And if their HQ treasury team is still operating with limited staff and no dedicated treasury solution, this rise in complexity represents a monumental strain on bandwidth. With more banks, accounts, payments, and currencies to track, as well as new tax and compliance considerations (not to mention fraud and cybercrime exposure), bank portals and Excel are no longer sufficient for managing the enterprise’s global web of activity. Instead, these overly manual processes will put pressure on the entire company and ultimately hinder the financial operations of other departments, including the C-suite, as key payments and liquidity data take days or even weeks to ascertain.

It is at this stage of company growth that the need for an advanced treasury and payments solution becomes much more obvious.

However, even as companies come to this realization, finding and deploying the best-fit solution can be difficult. Due to the broad variety of vendors and solutions in the market, along with the disparity in formats, channels, and networks that manifest themselves within growing companies over time, creating a modernized treasury stack usually requires a sophisticated technical review and implementation(s). And for already understaffed treasury and IT groups that lack the bandwidth and resources to manage these projects on their own, the task of performing due diligence and vetting vendors can be a laborious one.

But then, given these constraints, what is the best way for fast-growing companies to manage the selection and adoption of new treasury technology without becoming more overwhelmed?

How Scaling Companies Can Identify & Implement the Best-Fit Treasury Platform

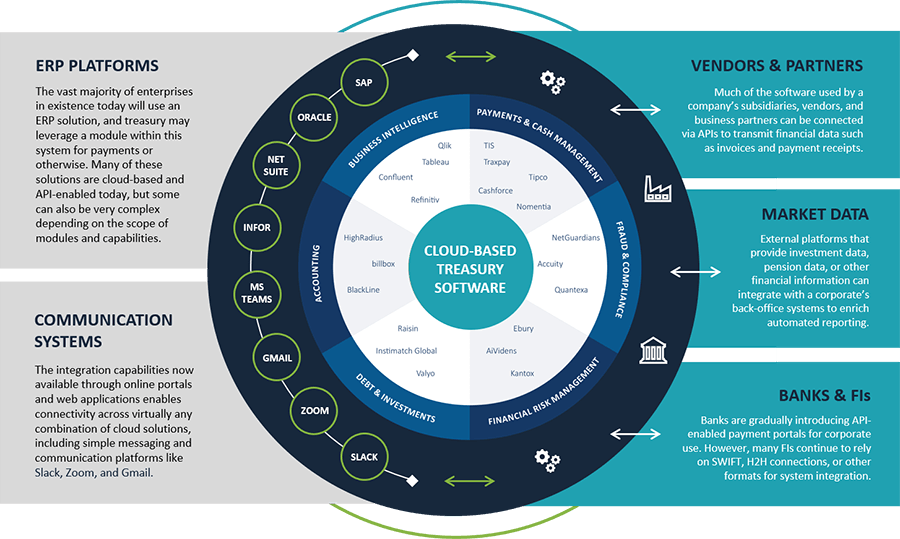

For companies in a situation similar to the above example, there are a variety of technologies available to help optimize treasury and payments functions. These include ERP treasury modules, TMS platforms, enterprise payment hubs, internal IT systems, corporate banking solutions, and more. There are also dozens (if not hundreds) of vendors operating across each of these categories. And as already mentioned, this broad range of potential solutions can make selection projects quite difficult.

Despite these complications, however, it’s important for treasury to take the process seriously. Given the rate of change in today’s technology environment, finding a long-term and sustainable solution that can accommodate future growth requires a thorough analysis of your own processes and needs, as well as extensive due diligence of the technology industry and its associated vendors. This means that in addition to assessing the functional needs of your treasury group, other departmental stakeholders, and various local personnel, you must also evaluate the evolving solutions’ landscape and its preeminent trends.

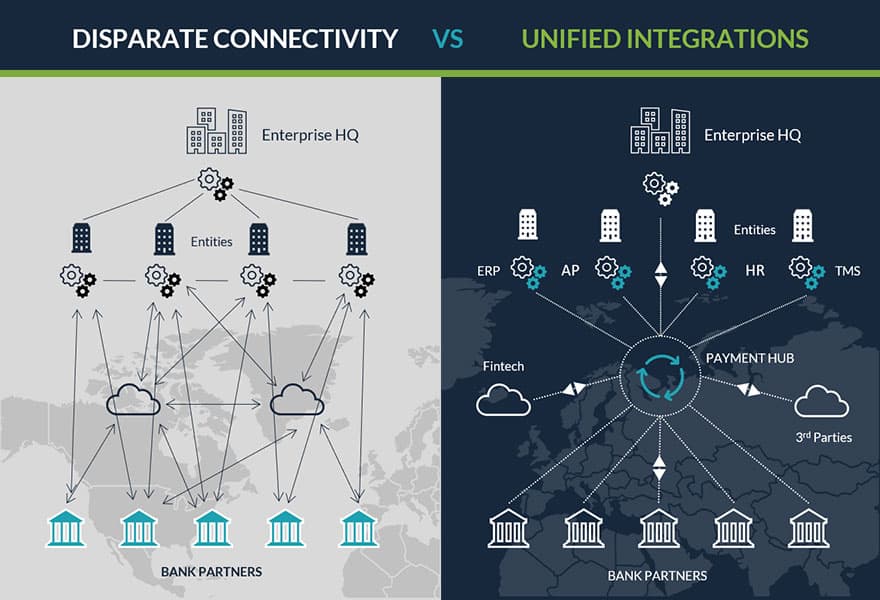

For instance, while onsite or “locally hosted” ERP and TMS platforms were popular in the early 2000s, now in 2021, the overwhelming majority of new technology implementations are of cloud-based, open API solutions. As compared to their predecessors, these solutions are usually hosted offsite by the vendors themselves.

Why?

Because the myriad of 3rd party, back-office, and bank systems that enterprises are using is under constant flux, the adoption of vendor-hosted cloud platforms enables enterprises to outsource the process of connecting their systems to the vendors, who subsequently develop data-sharing workflows through APIs, plugins, and H2H / “direct” connections. This is a massive plus for enterprises that use numerous systems but that don’t have the IT bandwidth, technology knowhow, or desire to build and maintain the connections inhouse.

Other technology-oriented evaluations would include the use of various security protocols and data privacy techniques, as well as the compatibility with global payments formats, bank channels, and reporting standards.

When combined with the more functional aspects of treasury’s technology focus (i.e. the actual financial and analysis capabilities provided through the system), these operational elements help form the basis on which potential technology solutions are evaluated.

The following summary outlines these core technology adoption considerations in more detail.

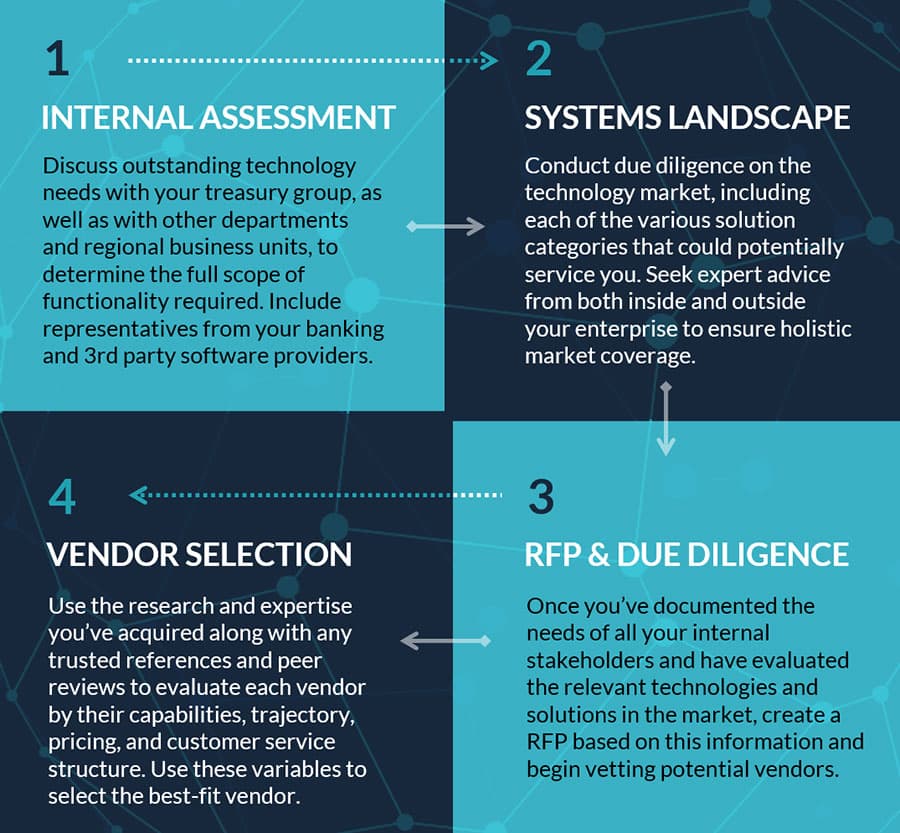

- Consider ALL Internal Needs: Discuss the project with your treasury group, as well as with other departments and regional business units, to determine the scope of functionality required. Include representatives from your banking and 3rd party software providers to better understand how the flow of data and information between these systems and your global offices and entities must be configured.

- Evaluate Technology Landscape: Conduct due diligence on the technology market, including each of the various solution categories that could potentially service you (i.e. TMS, ERP, bank, Payment Hub, IT, etc.) Seek expert advice from both inside and outside your enterprise to determine the full scope of available solutions and the anticipated trajectory of each solution category.

- Submit RFPs & Evaluate Vendors: Based on the evaluation of your enterprise’s needs and on ample due diligence of the technology market, submit RFPs to relevant vendors and begin evaluating their ability to service your company.

- Manage Implementation & Subsequent Use: Use the research and expertise you’ve acquired to evaluate your list of vendors by their capabilities, size, market trajectory, pricing, and customer service structure. It is also recommended to speak with references and peers during this process. Use these variables along with the strength and functionality of their solution set to narrow down your selection and ultimately choose the “best-fit” vendor.

In the end, the specific type of solution that is adopted by your company should vary based on your findings from the above process. Of course, as your company scales, the need for additional technology systems becomes a greater likelihood, and new systems may be implemented with more frequency. This is why the technology aspect of implementations are so important – by structuring your technology stack in a manner that promotes open connectivity and integration with other systems and banks, you’ll be able to seamlessly connect each new solution with your existing infrastructure. This will ensure that future growth can continue unimpeded without excess technology complexity getting in the way.

Learn More About TIS’ Enterprise Payment Platform

For growing companies that need help managing functions like bank connectivity, payments, cash positioning, and liquidity, we invite you to explore how TIS’ Enterprise Payment Optimization (EPO) platform can help optimize your workflows. For a full overview of our platform, click here. You can also learn more about how our platform helps simplify global technology infrastructures, how we help prevent fraudulent activity, and how we deploy the use of APIs in our solution to increase compatibility with other platforms. To request an information session with one of our product experts, click here.