This article reviews the core mechanics of Supply Chain Finance (SCF) and evaluates how modern innovations in technology and financing options are impacting the various buyers, suppliers, banks, and fintech vendors that have a stake in the process. After highlighting the fundamental strategies and workflows associated with SCF, we will examine how today’s most popular SCF solutions for reverse factoring and dynamic discounting influence the working capital and liquidity operations of participating organizations and institutions.

Supply Chain Finance 101: Key Concepts

Although the technologies and workflows associated with supply chain financing (SCF) are under constant evolution, the fundamental practices of adjusting payment terms and establishing credit between different parties in the supply chain has remained largely the same for thousands of years.

At its core, SCF is nothing more than a variation in the payment terms between a buyer and seller in the supply chain that either extends or shortens the timeframe that goods and services (i.e., invoices) are paid for. Typically, SCF programs provide incentives for buyers to pay their supplier invoices early or as quickly as possible by offering discounts for early payment. However, other types of SCF programs can instead provide buyers the chance to delay payment for as long as possible in order to hold onto their cash, while simultaneously providing suppliers with capital via bank credit or financing.

At its core, SCF is nothing more than a variation in the payment terms between buyers and sellers in the supply chain that either shortens or extends the timeframe that goods and services are paid for.

Over the past few decades, there have been a variety of adaptations and variations to traditional supply chain finance that have permeated the global business landscape. Today, supply chain finance programs can be created and managed by both buyers and suppliers, as well as by 3rd party financiers and banks. The majority of modern programs also involve fintech vendors that provide software and online applications for connecting all parties in the supply chain together for added automation and visibility. But while each financing program and platform may differ slightly in how it is executed and which parties are ultimately involved, the intent and purpose of all programs are the same in that they provide opportunities for participants in the supply chain to improve their working capital positions by adjusting payment terms or establishing credit with one another.

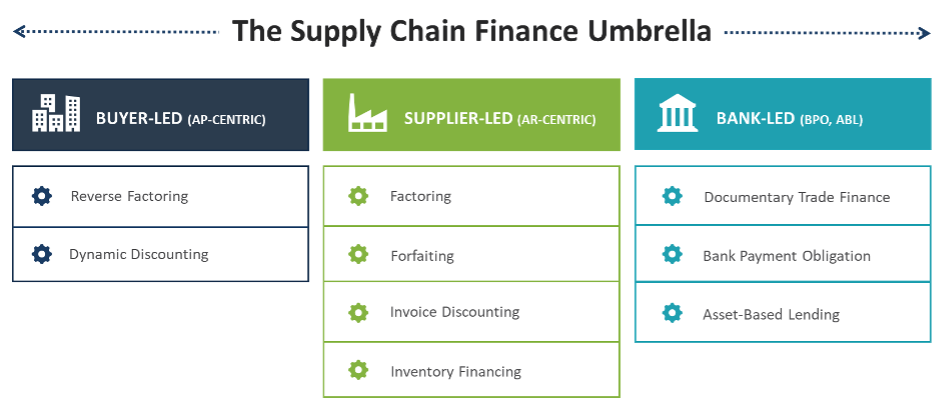

What are the Most Popular Forms of SCF in 2022?

As it stands today, many of the most prevalent SCF strategies are buyer-led, AP-centric programs such as Reverse Factoring and Dynamic Discounting. These programs are considered “buyer-led” because it is normally large enterprise buyers that jumpstart them and offer participation to their global network of suppliers. And because it is the buyer’s accounts payables (i.e., outstanding invoices) that the SCF program revolves around, they are considered “AP-centric” strategies.

Overviews of both reverse factoring and dynamic discounting workflows are provided below.

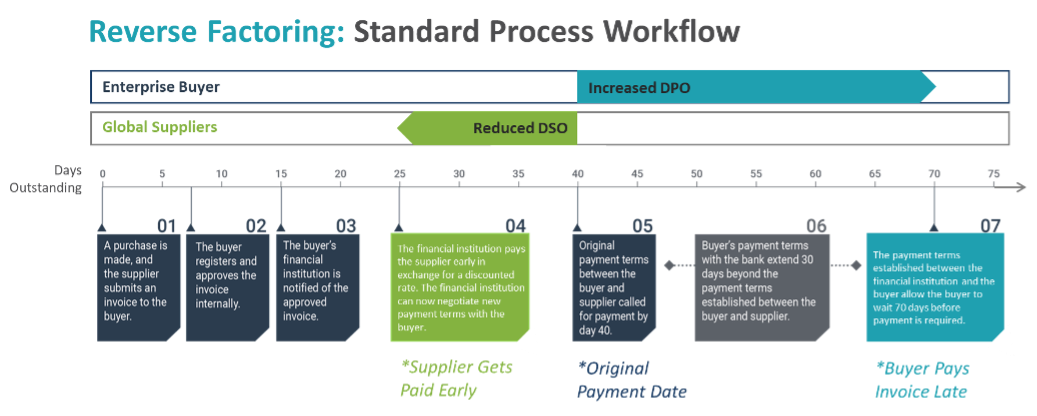

Reverse Factoring

Reverse factoring programs typically consist of a large enterprise buyer, a portion of their global supplier network, a bank or 3rd party financier(s), and a Fintech solutions vendor (optional).

Reverse factoring is widely regarded as the most popular and traditional form of supply chain finance. Using a reverse factoring program, an enterprise buyer will first partner with a bank or other 3rd party financier. Next, they will look to onboard portions of their supplier network. Then, as the buyer receives invoices from participating suppliers, they are delivered to the bank, which then pays the suppliers early (but at a discount) on behalf of the buyer. The buyer is then free to negotiate their own payment terms with the bank for paying back the full invoice amount, and will usually delay payment for as long as possible in order to hold onto their cash for as long as possible. The numbered list and graphic below highlight this workflow in more detail.

- A buyer partners with a bank or 3rd party financier that will ultimately be responsible for extending credit to the buyer’s suppliers for early payment of invoices.

- Once the buyer and financier agree to terms, the buyer will then look to onboard a portion of their suppliers to the program for participation. It is typically the most creditworthy suppliers that are offered participation first, but may extend to the “long-tail” of suppliers also.

- As suppliers are vetted and onboarded, there is typically an online platform, either hosted by the bank or a fintech vendor, that enables all parties to centrally connect and manage SCF workflows related to invoice uploading, payment approval, data transmission, etc.

- As new invoices are submitted by participating suppliers to the buyer for payment, the buyer transfers them immediately to the bank or financier. The financier then pays the suppliers earlier than the stated terms (i.e., in 10 days instead of 60), but in return for a small discount (i.e., 2-3%) of the total payment amount.

- Once the bank has paid the supplier invoice early at a discounted rate, the buyer and bank can then negotiate their own payment terms. Ultimately, the buyer will pay the bank the full invoice amount, but will wait as long as possible to do so (i.e., 60-75 days).

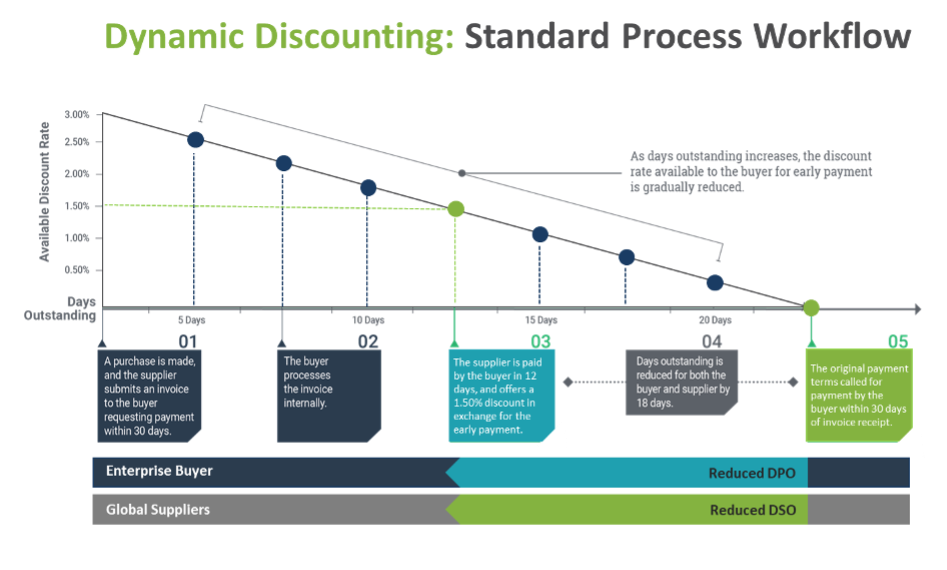

Dynamic Discounting

Dynamic discounting programs typically consist of an enterprise buyer, their global supplier network, and a Fintech solutions vendor.

Dynamic Discounting is similar to Reverse Factoring in the sense that suppliers are still getting paid early for their invoices at a discounted price. However, the difference is that the buyer is typically paying their suppliers directly, rather than relying on a bank to provide financing. The benefit for the buyer in this scenario is that they receive the discount offered by the supplier for early payment, instead of allowing a bank or financier to provide early payment and subsequently reap the discount themselves.

The reason this strategy is referred to as “dynamic discounting” is because the size of the discount offered by suppliers is commensurate with how quickly the invoice can be paid by the buyer. For instance, if an invoice has payment terms of 60 days but the buyer pays in 5 days, they will receive a larger discount from the supplier (i.e., 3%) than if they paid in 10 days (2%) or 15 days (1%). Over time, the size of the discount offered for early payment is diminished, so that after 60 days, there is no discount remaining, and the buyer must pay the invoice back in full.

Dynamic discounting differs from traditional “2/10, n30” discounts because the size of the discount is constantly changing over time, as opposed to a flat-rate discount if payment is provided before a certain cut-off date. With dynamic discounting, the buyer always has an incentive to pay early, and so the supplier stands a better chance of receiving funds early, albeit for a slight discount.

How Does SCF Help Maximize Working Capital Efficiency for Each Participant?

Through the use of modern-day supply chain financing, each of the involved parties – from the buyers and suppliers to the banks and technology vendors — stand to benefit.

Buyers & Large Enterprises: For large businesses that extend supply chain financing to hundreds or even thousands of their suppliers, the benefits of working capital can be immense. When using a reverse factoring program, the main benefit is that the enterprise can extend the timeframe for paying invoices, which means they can effectively hold onto cash for longer in order to invest it elsewhere, or to satisfy other payment obligations. If the enterprise is regularly able to wait 60-75+ days to pay invoices compared to 10-30 days, they have a 2-3x longer runway to maximize returns or leverage their cash for other purposes, which is hugely beneficial from a liquidity perspective.

Alternatively, enterprises that use a dynamic discounting program can choose to pay their suppliers early for a discount, rather than holding onto their cash for as long as possible. In this circumstance, the benefit is that they receive a discount on the amount owed per invoice, which can be equally as cost-effective as delaying the payment and investing or deploying their cash elsewhere.

Suppliers & Vendors: For traditionally small-and-mid-sized suppliers that participate in supply chain financing, the benefits are typically the same regardless of whether a reverse factoring or dynamic discounting program is used. In either case, the supplier’s invoices are being paid earlier than usual, but they receive payment at a discounted rate. However, because many small suppliers do not have the same credit ratings as large buyers, they often do not have access to capital or credit at the same rate. As a result, many suppliers are happy to leverage their buyer’s superior credit rating to receive 97-99% of what they are owed on each invoice within 10-15 days, as opposed to waiting 50-75 days to receive the full amount. The only component that differs is that in a reverse factoring program, the discounted early payment is provided via a bank financier, and in a dynamic discounting program, the discounted early payment comes directly from the buyer.

Although SCF is sometimes considered to only be attractive for small suppliers that need fast and affordable access to cash, there are circumstances where large, creditworthy suppliers are also willing to participate. This is usually the case if the supplier is growing quickly or has identified other opportunities to invest or deploy cash across their business, and wants invoices paid as quickly as possible in order to redeploy the funds. Provided that the ROI available to the supplier through these opportunities can make up for the discount afforded to the buyer or financier for early payment, supply chain financing will remain attractive for even the largest and most creditworthy suppliers.

Banks & Fintech Vendors: For banks and financiers that participate in SCF, the main benefit is that they earn a profit by paying a discounted rate on invoices to suppliers, and then receiving the total payment amount at a later date from the buyer. For instance, if the bank regularly pays a supplier in 10 days in exchange for a 3% discount on an invoice, and then receives full payment on the invoice from the buyer at on day 30, they effectively earn a 3% profit on the invoice over a 20-day period.

In addition to bank participation, there are also usually cloud-based software vendors that provide the technology and software through which buyers and suppliers can interact. Although these platforms are sometimes managed directly by banks, 3rd party fintech vendors have become popular hosts for these types of products. For these vendors, there are typically subscription and service fees associated with the use of their online system to facilitate SCF transactions, provide workflow automation and visibility, and to host and maintain the software. Examples of popular cloud-based SCF systems today include C2FO, Taulia, and PrimeRevenue.

How Technology Improves Working Capital Efficiency in Supply Chain Finance

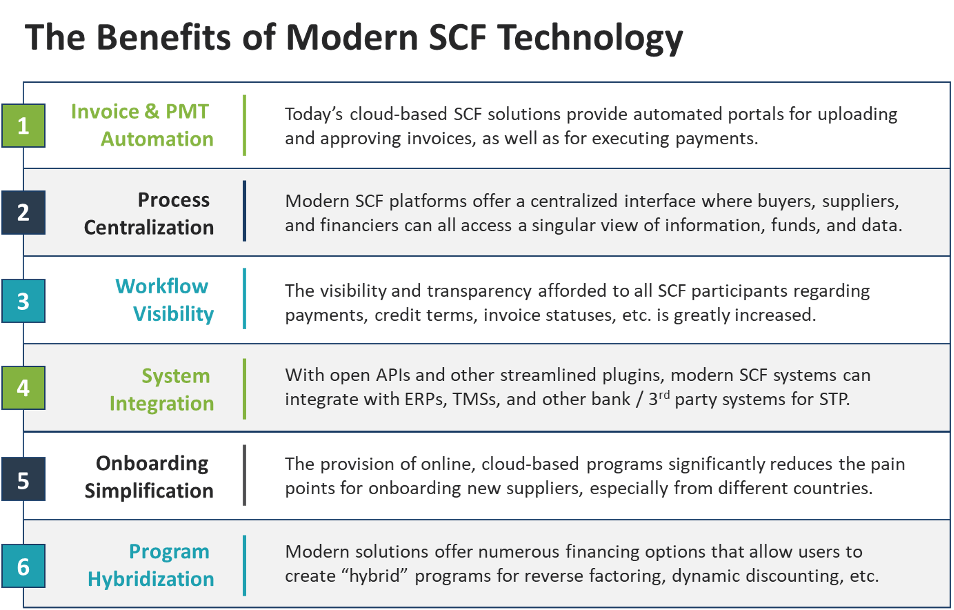

Today, the prevalence and accessibility of cloud-based SCF applications, open APIs, and digital automation tools have made global collaboration and participation in supply chain finance programs easier than ever before.

In the past, supply chain finance programs were constrained by a lack of automation and visibility because businesses were relying on siloed data systems or manual, paper-based processes. Without easily accessible and centralized systems where all invoicing, payment approval, compliance, and general data transmission could be managed, it was difficult to stay updated on what invoices were available for early payment, which payments had cleared, and which companies were actively participating, and so forth. Issues with supplier onboarding and participation were particularly difficult, as it took manual effort to vet and integrate new vendors, especially from different countries and regions with unique compliance and regulatory standards. As a result, most buyers would only focus on onboarding their largest and most trustworthy suppliers, and would leave the majority of their smaller “long-tail” suppliers (who were often most in need of financing) out of the program.

However, with the democratization of cloud-based SCF solutions that have occurred in recent years and the automation and visibility that can now be achieved, the breadth of capabilities and ease of access available to large enterprises and small suppliers alike have made supply chain financing monumentally more attractive.

Given the prevalence of cloud-based, open API solutions on the market today, the process of transmitting funds and data between SCF platforms and other back-office systems like ERPs and TMS systems can be largely automated. The same goes for the process of connecting with the systems used by banks and financiers. The result is that businesses can integrate their SCF program and platform with their back-office and banking landscape in order to have a singular view of payments, invoices, cash balances, and credit terms across all participating entities and parties.

In the near future, it is worth noting that blockchain and digital ledger technology (DLT) are likely to also play a greater role in supply chain finance, both as a means of record-keeping and also for facilitating transactions. In fact, there are a variety of solutions providers operating in this arena, as well as a small but growing number of organizations actively leveraging these products. However, there is still likely another 5-10 years to go before the adoption and use of such technology can be considered “mainstream”.

How TIS Helps Companies Optimize Their Supply Chain Finance Programs

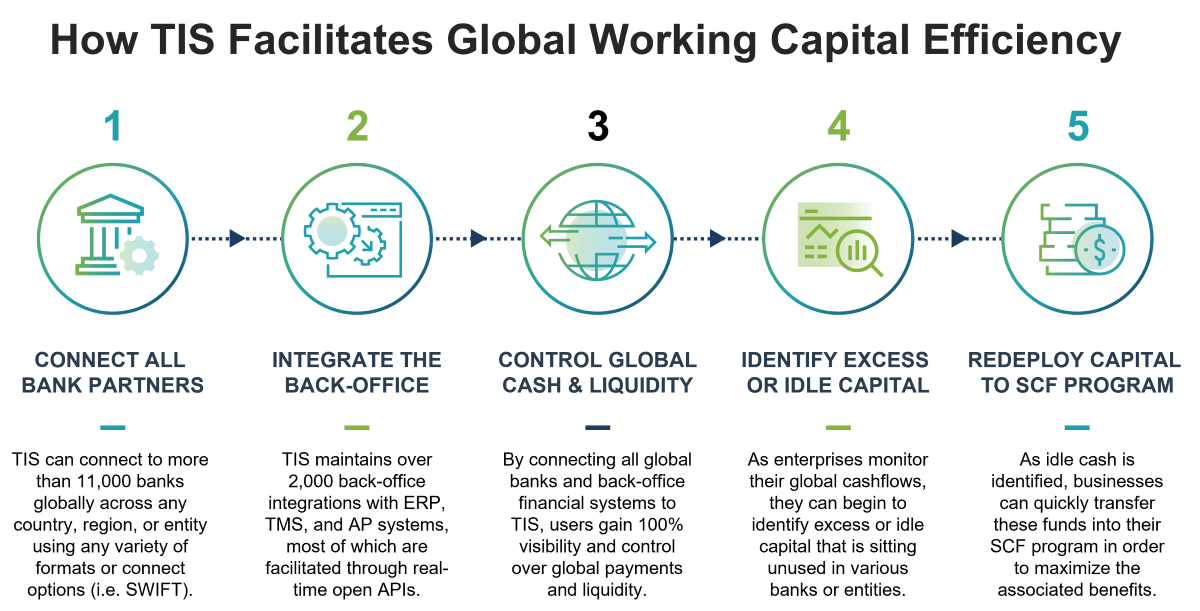

As it stands today, the use of TIS’ cloud-based payments and liquidity management platform in conjunction with an SCF solution can provide significant benefits.

To start, TIS’ platform specializes in connecting all of an enterprise’s global banks, accounts, and 3rd party platforms together for a unified view of payments and liquidity across every country, entity, and currency. As a result, enterprises that leverage TIS always have a complete, real-time picture of their cash positions and payment statuses. This 360-degree view, coupled with total control over payment generation and execution, is what ultimately enables our clients to refine and optimize their associated cash and working capital strategies.

As global payments, banking, and liquidity data is collected by TIS, information and funds can be quickly transmitted through TIS to other systems. For instance, TIS can help businesses identify excess cash in foreign bank accounts or business entities, and help redirect those funds into a supply chain finance solution in order to maximize working capital efficiency. Our automated payment execution and bank connectivity features also automate the transaction process so that funds can quickly be transmitted to other business areas.

By coupling TIS’ payments and liquidity hub with a cloud-based SCF solution, enterprises can achieve global visibility and control over their liquidity and payment workflows, which enables them to quickly identify and deploy idle capital into their SCF program. This ultimately boosts the value obtained through the SCF program and ensures that idle cash across the business is being identified and redeployed in order to maximize working capital efficiency. The methods and workflows through which these processes are accomplished are highlighted in the below graphic.

For enterprises interested in learning more about how TIS can be used to optimize global payments and liquidity processes, we invite you to visit our website resource hub or contact one of our experts for more information.